Extrapolate values in Pandas DataFrame

Extrapolating Pandas DataFrames

DataFrames maybe be extrapolated, however, there is not a simple method call within pandas and requires another library (e.g. scipy.optimize).

Extrapolating

Extrapolating, in general, requires one to make certain assumptions about the data being extrapolated. One way is by curve fitting some general parameterized equation to the data to find parameter values that best describe the existing data, which is then used to calculate values that extend beyond the range of this data. The difficult and limiting issue with this approach is that some assumption about trend must be made when the parameterized equation is selected. This can be found thru trial and error with different equations to give the desired result or it can sometimes be inferred from the source of the data. The data provided in the question is really not large enough of a dataset to obtain a well fit curve; however, it is good enough for illustration.

The following is an example of extrapolating the DataFrame with a 3rd order polynomial

f(x) = a x3 + b x2 + c x + d (Eq. 1)

This generic function (func()) is curve fit onto each column to obtain unique column specific parameters (i.e. a, b, c, d). Then these parameterized equations are used to extrapolate the data in each column for all the indexes with NaNs.

import pandas as pd

from cStringIO import StringIO

from scipy.optimize import curve_fit

df = pd.read_table(StringIO('''

neg neu pos avg

0 NaN NaN NaN NaN

250 0.508475 0.527027 0.641292 0.558931

500 NaN NaN NaN NaN

1000 0.650000 0.571429 0.653983 0.625137

2000 NaN NaN NaN NaN

3000 0.619718 0.663158 0.665468 0.649448

4000 NaN NaN NaN NaN

6000 NaN NaN NaN NaN

8000 NaN NaN NaN NaN

10000 NaN NaN NaN NaN

20000 NaN NaN NaN NaN

30000 NaN NaN NaN NaN

50000 NaN NaN NaN NaN'''), sep='\s+')

# Do the original interpolation

df.interpolate(method='nearest', xis=0, inplace=True)

# Display result

print ('Interpolated data:')

print (df)

print ()

# Function to curve fit to the data

def func(x, a, b, c, d):

return a * (x ** 3) + b * (x ** 2) + c * x + d

# Initial parameter guess, just to kick off the optimization

guess = (0.5, 0.5, 0.5, 0.5)

# Create copy of data to remove NaNs for curve fitting

fit_df = df.dropna()

# Place to store function parameters for each column

col_params = {}

# Curve fit each column

for col in fit_df.columns:

# Get x & y

x = fit_df.index.astype(float).values

y = fit_df[col].values

# Curve fit column and get curve parameters

params = curve_fit(func, x, y, guess)

# Store optimized parameters

col_params[col] = params[0]

# Extrapolate each column

for col in df.columns:

# Get the index values for NaNs in the column

x = df[pd.isnull(df[col])].index.astype(float).values

# Extrapolate those points with the fitted function

df[col][x] = func(x, *col_params[col])

# Display result

print ('Extrapolated data:')

print (df)

print ()

print ('Data was extrapolated with these column functions:')

for col in col_params:

print ('f_{}(x) = {:0.3e} x^3 + {:0.3e} x^2 + {:0.4f} x + {:0.4f}'.format(col, *col_params[col]))

Extrapolating Results

Interpolated data:

neg neu pos avg

0 NaN NaN NaN NaN

250 0.508475 0.527027 0.641292 0.558931

500 0.508475 0.527027 0.641292 0.558931

1000 0.650000 0.571429 0.653983 0.625137

2000 0.650000 0.571429 0.653983 0.625137

3000 0.619718 0.663158 0.665468 0.649448

4000 NaN NaN NaN NaN

6000 NaN NaN NaN NaN

8000 NaN NaN NaN NaN

10000 NaN NaN NaN NaN

20000 NaN NaN NaN NaN

30000 NaN NaN NaN NaN

50000 NaN NaN NaN NaN

Extrapolated data:

neg neu pos avg

0 0.411206 0.486983 0.631233 0.509807

250 0.508475 0.527027 0.641292 0.558931

500 0.508475 0.527027 0.641292 0.558931

1000 0.650000 0.571429 0.653983 0.625137

2000 0.650000 0.571429 0.653983 0.625137

3000 0.619718 0.663158 0.665468 0.649448

4000 0.621036 0.969232 0.708464 0.766245

6000 1.197762 2.799529 0.991552 1.662954

8000 3.281869 7.191776 1.702860 4.058855

10000 7.767992 15.272849 3.041316 8.694096

20000 97.540944 150.451269 26.103320 91.365599

30000 381.559069 546.881749 94.683310 341.042883

50000 1979.646859 2686.936912 467.861511 1711.489069

Data was extrapolated with these column functions:

f_neg(x) = 1.864e-11 x^3 + -1.471e-07 x^2 + 0.0003 x + 0.4112

f_neu(x) = 2.348e-11 x^3 + -1.023e-07 x^2 + 0.0002 x + 0.4870

f_avg(x) = 1.542e-11 x^3 + -9.016e-08 x^2 + 0.0002 x + 0.5098

f_pos(x) = 4.144e-12 x^3 + -2.107e-08 x^2 + 0.0000 x + 0.6312

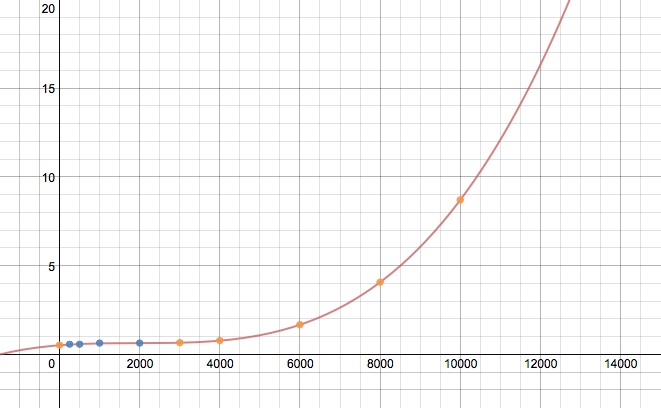

Plot for avg column

Without a larger dataset or knowing the source of the data, this result maybe completely wrong, but should exemplify the process to extrapolate a DataFrame. The assumed equation in func() would probably need to be played with to get the correct extrapolation. Also, no attempt to make the code efficient was made.

Update:

If your index is non-numeric, like a DatetimeIndex, see this answer for how to extrapolate them.

linearly extrapolate pandas dataframe using built-in interpolate method

You can use scipy interpolate method directly in pandas. See pandas.DataFrame.interpolate documentation, you can use in method option techniques from scipy.interpolate.interp1d as it's noted in the attached link.

Solution for your example could look like:

df.interpolate(method="slinear", fill_value="extrapolate", limit_direction="both")

# Out:

# 0

# 0 -7.0

# 1 -3.0

# 2 1.0

# 3 5.0

# 4 5.5

# 5 6.0

# 6 6.1

# 7 6.2

# 8 6.3

You can then easily select any values you are interested in, e.g. df_interpolated.loc[x] (where df_interpolated is output of the previous code block) using indexes defined in your question by x variable.

Explanation:

method="slinear"- one of the method listed in pandas doc above that is passed to scipyinterp1d(see e.g. this link)fill_value="extrapolate"- pass any option allowed by scipy (here extrapolate which is exactly what you want)limit_direction="both"- to get extrapolation in both direction (otherwise default would be set to "forward" in that case and you would seenp.nanfor the first two values)

Linear extrapolation in dataframes

I did something similar a while ago. It isn't super pretty, but maybe you can use it. As an example I'm using the following DataFrame (modified version of your second example):

value

year

2009 NaN

2010 NaN

2011 NaN

2012 320700.0

2013 315300.0

2014 310500.0

2015 307500.0

2016 315400.0

2017 NaN

2018 NaN

2019 NaN

year is the index!

The 1. step is filling up the end piece of NaNs:

increment = df.value.diff(1).mean()

idx_max_notna = df.value[df.value.notna()].index.array[-1]

idx = df.index[df.index >= idx_max_notna]

df.value[idx] = df.value[idx].fillna(increment).cumsum()

Result:

value

year

2009 NaN

2010 NaN

2011 NaN

2012 320700.0

2013 315300.0

2014 310500.0

2015 307500.0

2016 315400.0

2017 314075.0

2018 312750.0

2019 311425.0

As increment I've used the mean of the existing diffs. If you want to use the last diff then replace it with:

increment = df.value.diff(1)[df.value.notna()].array[-1]

The 2. step of filling up the start piece of NaNs is more or less the same, just with the column value reversed, and at the end re-reversed:

df.value = df.value.array[::-1]

increment = df.value.diff(1).mean()

idx_max_notna = df.value[df.value.notna()].index.array[-1]

idx = df.index[df.index >= idx_max_notna]

df.value[idx] = df.value[idx].fillna(increment).cumsum()

df.value = df.value.array[::-1]

Result:

value

year

2009 324675.0

2010 323350.0

2011 322025.0

2012 320700.0

2013 315300.0

2014 310500.0

2015 307500.0

2016 315400.0

2017 314075.0

2018 312750.0

2019 311425.0

Important: The method assumes that there is no gap in the index (missing year).

As I said, not very pretty, but it worked for me.

(PS: Just to clarify the use of 'similar' above: This is indeed linear extrapolation.)

EDIT

Sample frame (the first 3 rows of the frame in the screenshot):

n2hn_df = pd.DataFrame(

{'2010': [134.024, np.NaN, 36.711], '2011': [134.949, np.NaN, 41.6533],

'2012': [128.193, np.NaN, 33.4578], '2013': [125.131, np.NaN, 33.4578],

'2014': [122.241, np.NaN, 33.6356], '2015': [115.301, np.NaN, 35.5919],

'2016': [108.927, 520.38, 40.1008], '2017': [106.101, 523.389, 41.38],

'2018': [96.1861, 526.139, 49.0906], '2019': [np.NaN, np.NaN, np.NaN]},

index=pd.Index(data=['AT', 'BE', 'BG'], name='NUTS_ID')

)

2010 2011 2012 ... 2017 2018 2019

NUTS_ID ...

AT 134.024 134.9490 128.1930 ... 106.101 96.1861 NaN

BE NaN NaN NaN ... 523.389 526.1390 NaN

BG 36.711 41.6533 33.4578 ... 41.380 49.0906 NaN

Extrapolation:

# Transposing frame

n2hn_df = n2hn_df.T

for col in n2hn_df.columns:

# Extract column

ser = n2hn_df[col].copy()

# End piece

increment = ser.diff(1).mean()

idx_max_notna = ser[ser.notna()].index.array[-1]

idx = ser.index[ser.index >= idx_max_notna]

ser[idx] = ser[idx].fillna(increment).cumsum()

# Start piece

ser = pd.Series(ser.array[::-1])

increment = ser.diff(1).mean()

idx_max_notna = ser[ser.notna()].index.array[-1]

idx = ser.index[ser.index >= idx_max_notna]

ser[idx] = ser[idx].fillna(increment).cumsum()

n2hn_df[col] = ser.array[::-1]

# Re-transposing frame

n2hn_df = n2hn_df.T

Result:

2010 2011 2012 ... 2017 2018 2019

NUTS_ID ...

AT 134.024 134.9490 128.1930 ... 106.101 96.1861 91.456362

BE 503.103 505.9825 508.8620 ... 523.389 526.1390 529.018500

BG 36.711 41.6533 33.4578 ... 41.380 49.0906 50.638050

How to extrapolate missing values with groupby - Python?

You can modify the linked answer as follows:

def extrapolate(df):

new_max = df.index.max() + pd.to_timedelta('30D')

dates = pd.date_range(df.index.min(), new_max, freq='D')

ret_df = df.reindex(dates)

x = np.arange(len(df))

# new x values

new_x = pd.Series(np.arange(len(ret_df)), index=dates)

for col in df.columns:

fit = np.polyfit(x, df[col], 1)

# tranform and fill

ret_df[col].fillna(fit[0]*new_x + fit[1], inplace=True)

return ret_df

and then apply:

ext_cols = ['value_1', 'value_2']

df.groupby('account_id')[ext_cols].apply(extrapolate)

You can also specify the polynomial orders for each column:

poly_orders = [1,2]

ext_cols = ['value_1', 'value_2']

def extrapolate(df):

new_max = df.index.max() + pd.to_timedelta('30D')

dates = pd.date_range(df.index.min(), new_max, freq='D')

ret_df = df.reindex(dates)

x = np.arange(len(df))

# new x values

new_x = pd.Series(np.arange(len(ret_df)), index=dates)

for col, o in zip(ext_cols, poly_orders):

fit = np.polyfit(x, df[col], o)

print(fit)

# tranform and fill

new_vals = pd.Series(0, index=dates)

for i in range(1,o+1):

new_vals = new_x**i * fit[o-i]

ret_df[col].fillna(new_vals, inplace=True)

return ret_df

And use sklearn.linear_model.LinearRegression for better manipulation of input/output instead of numpy.polyfit.

pandas extrapolation of polynomial

"With the same elegance" is a somewhat tall order but this can be done. As far as I'm aware you'll need to compute the extrapolated values manually. Note it is very unlikely these values will be very meaningful unless the data you are operating on actually obey a law of the form of the interpolant.

For example, since you requested a second degree polynomial fit:

import numpy as np

t = df["time"]

dat = df["data"]

p = np.poly1d(np.polyfit(t,data,2))

Now p(t) is the value of the best-fit polynomial at time t.

Related Topics

Does Python Have a Stack/Heap and How Is Memory Managed

Making Heatmap from Pandas Dataframe

Convert Columns to String in Pandas

Convert a List with Strings All to Lowercase or Uppercase

On Localhost, How to Pick a Free Port Number

Conda Command Is Not Recognized on Windows 10

How to Get a Complete List of Object's Methods and Attributes

How to Manage Third-Party Python Libraries with Google App Engine? (Virtualenv? Pip)

Check If a Number Is Int or Float

Why am I Getting Importerror: No Module Named Pip ' Right After Installing Pip

How to Write a File or Data to an S3 Object Using Boto3

Salt and Hash a Password in Python

Python Eval: Is It Still Dangerous If I Disable Builtins and Attribute Access

Selenium: Firefoxprofile Exception Can't Load the Profile

Cannot Pass an Argument to Python with "#!/Usr/Bin/Env Python"

How to Check If a Value Is in the List in Selection from Pandas Data Frame

Python Lookup Hostname from Ip with 1 Second Timeout

What's the Difference Between Str.Isdigit, Isnumeric and Isdecimal in Python